I write about sports gambling around here more than I used to, because sports gambling has become pretty closely integrated with postmodern financial markets. Sometimes, when I write about sports gambling, I get emails from readers explaining that sportsbooks set their betting lines to balance bets on each side: A sportsbook sets the odds or point spread of a game so that it will pay the same amount of money regardless of which team wins. The book will collect, say, $100 of bets on the favorite and $50 of bets on the underdog, and it will set its odds to pay out $140 if the favorite wins and $140 if the underdog wins, keeping $10 — the “vig” — for itself in either case.

This is a popular view of sports betting, but it is wrong. It’s not entirely wrong: Sensible sportsbooks will manage risk and try to keep the action somewhat balanced. But in fact many sportsbooks regularly make directional bets on outcomes: They have some view of the likely result, and they set their odds to, in effect, bet on the more likely outcome. See “The Logic of Sports Betting” by Ed Miller and Matthew Davidow, particularly the chapter on “Market Making.” See also this Las Vegas Review-Journal column from 2022, and discussions at Altenar and Pinnacle. There is some simplification here, and e.g. Nate Silver (following Miller and Davidow) distinguishes market-making books (which take more risk and don’t focus on balance) from retail books (which limit bettors more and try harder to be balanced). And then sometimes they lose money on a game, and other times they win money on a game, but if their models are good they win more than they lose and are more profitable than they would be if they always balanced bets exactly. Intuitively, the general public is systematically wrong — people tend to irrationally bet on their home teams, underdogs, etc. — and taking the other sides of those bets is generally profitable. The sportsbook might stay “close to home” (not too much risk either way), but it doesn’t have to be “flat” (no risk either way). It is not looking to take no risk; it’s looking to take the right risk. This is perhaps most obvious in parlays, the big money-maker for modern sportsbooks. A parlay is, like, if some menu of 12 events happens in a basketball game, your $10 bet pays off $10,000, but if any of the events fails to occur you lose your $10. Obviously the sportsbook is not balancing your $10 parlay bet against 1,000 other bettors betting $10 to win $0.001 if any one event fails to occur: The sportsbook is taking that risk itself.

Loosely speaking, the role of bookies in the stock market is played by electronic proprietary trading firms. “Prop trading firm” is sort of a generic name for these firms, though “market maker” or “dealer” will also sometimes be used to describe this liquidity-providing function. And there are prop trading firms that don’t do any market making and just make directional bets. If a retail investor wants to buy a stock, she will probably buy it from Citadel Securities or Hudson River Trading or Virtu or Jane Street or someone like that. Those trading firms will sell some stock to one retail investor one second, and buy some stock from a different retail investor a second later.

You could imagine the trading firms working more like the popular perception of bookies, or more like actual bookies. That is:

Trading firms might buy 100 shares of Stock A one second and sell 100 shares of Stock A the next second. Over a second or two, they might be long or short Stock A. But over the long run, they try very hard to stay “close to home,” and every night they “go home flat,” with no net positions in any stocks. They make money only by capturing bid/ask spreads in short-term trading.

Trading firms might have some fundamental model of value, and if people want to sell Stock A below its fair value they will keep buying. If a firm accumulates 10,000 shares of Stock A during the course of the day, that’s fine. If it holds those shares overnight, or for days at a time, that’s fine. The point is not to be flat, but to be right. If the trading firm is systematically long stocks that go up and short stocks that go down, then that’s much more profitable than staying flat.

As with actual bookies, the truth is mostly somewhere in between. A lot of proprietary trading firms will have some model view of value, and will try to buy stocks below their value and sell above their value. They will have other constraints — risk limits, capital, etc. — that tend to push them to be close to home. The result will be a trading book that has much less directional risk than, you know, Bill Ackman’s portfolio. If an electronic trading firm had large long positions in 12 stocks and held them for months, that would be odd. But there can be some directional risk: If a trading firm ends each day with zero net position in every stock, it is leaving some money on the table.

Things are a bit easier for stock trading firms than they are for sportsbooks, in that financial markets have a lot of correlated instruments that can hedge each other. If a firm is long $100 of Stock A and short $100 of Stock B, that might be less risky than either position on its own: If Stocks A and B are correlated, their moves will mostly offset each other, and the firm is unlikely to lose anything close to the full $200. Or an options trading firm can hedge its options position with the underlying stock — long call options on 100 shares of Stock A, short 60 shares of Stock A to hedge — and won’t make or lose much money whichever way the stock moves. A stock market maker can have a lot of long positions and a lot of short positions and still feel, on balance, close to home.

This is harder for a sportsbook: We have talkedNo direct match for the specified Bloomberg article "openai doesn t want ai cheaters" (from the URL slug dated January 29, 2025) was found in the search results. Search results discuss related AI cheating topics, such as OpenAI allegedly manipulating math/reasoning benchmarks without much attention, AI enabling student plagiarism caught by professors, a consulting partner using AI to cheat on an internal AI training course, and AI not being the primary cause of cheating despite easing it. These do not provide the content of the Bloomberg opinion piece, which may be paywalled or not indexed here. No summary of the target article is possible from available data. [read] around here about sportsbook correlation models, but they have limited applicability (same-game parlays); as far as I know it is hard to hedge a bet on the Yankees with a bet on the Mets, or on the Masters for that matter. Financial assets tend to move together based on underlying economic factors; baseball games do not. There is no obvious reason that the result of the Mets game would tell you anything about the result of the Yankees game. It would be cool to be wrong about this, and if you’re trading a factor model of sports bets please be in touch.

Really, there is a range of these electronic proprietary trading firms: Some take very little directional risk and try to go home flat in everything most days; others have more complex hedging models that allow them to take lots of individual risks while keeping overall risk low; others will make unhedged billion-dollar directional bets if the expected value is good enough. There are a number of ways to read Jane Street’s Indian options trade, but one is perhaps “Jane Street liked to make large directional bets against Indian retail options traders, because Indian retail options traders were systematically wrong.” Again: There are other ways to read it.

Anyway, one reason I write a lot about sports gambling now is because I write a lot about prediction markets, which are sort of legally financial markets (in the US, they are commodity futures markets regulated by the Commodity Futures Trading Commission) but practically sportsbooks (79% of volume on KalshiNo Bloomberg article exactly titled "79% of volume on Kalshi" was found in search results, but related coverage references a Bank of America (BofA) report highlighted in the provided URL slug about a $1.1 trillion U.S. sports event betting market. According to summaries, BofA analyst Julie Hoover describes Kalshi as the fastest-growing company outside the AI sector, with weekly trading volume surging from $100 million to over $30 billion, capturing over 90% of the U.S. prediction market share. By March 2026, sports event contracts drove 79%-80% of Kalshi's platform volume, following initial growth from the 2024 election, while reliance on partners like Robinhood dropped from 60% in Q2 2025 to 23% as its direct-to-consumer platform strengthened. Polymarket and Kalshi together hold about 79% of the overall prediction market as of early 2026, with Kalshi's volume heavily concentrated in sports amid annual trading exceeding $44 billion industry-wide. [read] is sports bets). One frequently remarked difference between a prediction market and a traditional sportsbook is that, at a sportsbook, customers are betting against the sportsbook, while in a prediction market they are betting against each other.

I tend to be unimpressed by that difference, because it is also true of the stock market: Anyone can buy stock, and anyone can sell stock, so when you buy a share of stock you might theoretically be buying it from some other investor who wants to sell. But in practice you are almost certainly buying it from an electronic trading firm, because those are the firms that make markets on the stock exchange (and, more relevantly, for your retail brokerage The Bloomberg opinion article argues that the Robinhood-GameStop trading saga highlights flaws in payment for order flow (PFOF), a practice where brokers like Robinhood sell customer orders to market makers (e.g., Citadel) for rebates, enabling commission-free trading but potentially harming retail investors. It critiques how PFOF obscures execution costs from users—disclosures are aggregated and vague, making it hard for individuals to see if their orders received suboptimal prices—while fueling broker growth amid the meme-stock frenzy. Robinhood defends PFOF as uniform across market makers, prioritizing best execution quality and replacing old commission models, though critics like lawmakers question if it truly benefits everyday traders over institutional players. [read]). They are posting orders to buy and orders to sell, and if you want to sell or buy you will probably trade with their orders.

Similarly, in prediction markets, in the long run, it seems entirely plausible that customers will mostly trade with market makers: Professional electronic trading firms will post bids and offers on the prediction markets, and if you want to buy a contract you will in most cases buy from a trading firm that sells it. If the contract you want to buy is “Mets win tonight,” you will buy it from a trading firm that is in effect betting on the Mets losing. And then if someone else wants to buy “Mets lose,” they will also buy it from that trading firm, which will be trading on both sides of the market.

But:

We’re not there yet: There are some professional prediction-market traders who provide liquidity, but they do not yet seem to dominate volumes on the big prediction markets.

Who will these market makers be? There are some reasons to think that they will be the same prop trading firms that trade stocks and options and futures: Those firms are good at trading regulated financial assets, and prediction markets are regulated financial assets. But there are also some reasons to think that they will be the same sports market makers that make odds for sportsbooks: Those firms are good at trading sports bets, and prediction markets are sports bets. (Of course there is overlap; Susquehanna famously does both.)

If the market makers are traditional prop trading firms, they will have some difficulties an adapting to prediction markets, because the traditional correlation and hedging math of financial markets might not work as well in sports or other events.

There are numerous reasons why institutional traders have not joined in, including the lack of regulatory clarity and the relatively light volumes compared with the other areas where they operate.

But a new academic paper points to another potential reason: Some of the basic tools that sophisticated traders use to manage risk in other markets aren’t available in event-based bets.

At the most basic level, most market makers offset their risk in one type of trading by hedging with other related assets — for options markets, they can do this in the underlying stock market. That is much less easy when the bet is on a celebrity wedding or an election, according to the paper published by Nick Palumbo, a former product manager at the sports betting site DraftKings Inc.

Here is Palumbo’s paper, “A Microstructure Perspective on Prediction Markets,” finding that market makers on prediction markets don’t really earn bid/ask spreads so much as they make directional bets on events:

Passive liquidity providers systematically absorb residual demand imbalances and retain outcome-dependent exposure through contract resolution. Profitability appears to depend less on classical bid-ask spread capture and more on managing terminal risk associated with dynamic supply creation. These findings suggest that liquidity provision in event-contract markets shares structural similarities with underwriting rather than traditional inventory-neutral intermediation.

I guess my point would be that neither sports bookmaking nor stock prop trading is entirely “traditional inventory-neutral intermediation”; Jane Street does not just earn a bid/ask spread on all of its trades. From his findings:

Across the full NFL season:

Passive liquidity providers accumulated net exposure in the direction of realized outcomes in the majority of markets

In most cases, they had a terminal asset on one outcome and a terminal liability on the other

Aggregate profitability was positive (approximately $29 million)

On average, the sum of terminal assets was greater than the sum of terminal liabilities

Weekly P&L exhibited significant volatility, with pronounced drawdowns during adverse weeks

LPs [liquidity providers] are winning on average, but are not without weeks of significant losses

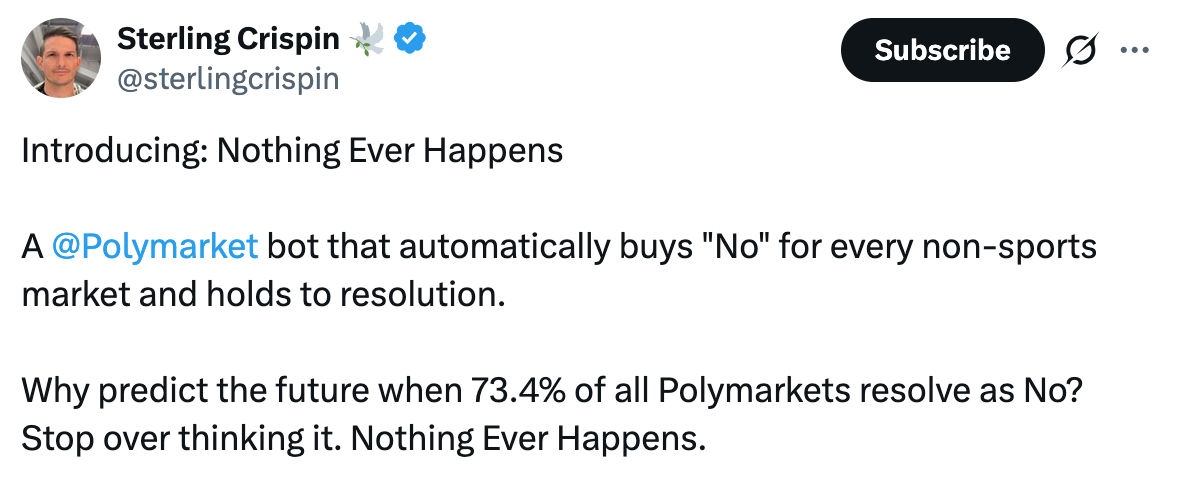

Yeah I mean seems fine? The job is to make markets where you have a positive expectation, and to win more than you lose.

Right, see, that’s (one-sided) model-based positive-expected-value Not investing advice! “Many things can and will go wrong if you run this bot unmodified,” notes Crispin. passive liquidity provision.

Prediction market resolution

In general, event contracts on prediction markets pay $1 if an event happens and $0 if it doesn’t. But how do you know, in general, if an event has happened? Or rather, how does the prediction market know: How does it decide whether to pay out the Yes contracts or the No contracts?

There are some events that have official results. Major League Baseball has a mechanism for deciding the winner of the Mets game, and a sportsbook or prediction market will probably defer to the official mechanism. The Oscars have official results. US elections, so far, have had official results. But most events in the world do not have official results. There is no official objective arbiter of whether US ground troops have entered Iran. The people who might know — the US military, the Iranian military — might not want to tell you. Or — as we discussed last week — you might know all the facts, but still not be sure whether those facts mean that “US ground troops have entered Iran” in the relevant sense.

So who decides, and how? The most straightforward answer would be something like:

The prediction market is a regulated financial exchange with a lot of lawyers.

The prediction market appoints a committee of lawyers and philosophers to decide whether events have occurred. Or, like, multiple committees, one for sports, one for entertainment, one for elections, one for war, etc., with relevant domain expertise.

They try to do a good job.

If they do a bad job, the prediction market loses customers, or regulators step in.

The committee evolves a code of ethics: Committee members aren’t allowed to trade themselves, or take bribes, etc.

The committee evolves a set of rules to make the substantive decisions. Each time some event contract has a difficult and controversial determination, the committee changes the rules for future event contracts to make the resolution easier and less controversial. If the “Cardi B performs at the Super Bowl” contract settles ambiguously because Cardi B danced and mouthed words but might not have been singing, you write future “_____ performs at _____” contracts to avoid that ambiguity. You do this over and over again, incrementally fixing rough patches, so that, in 10 years, prediction markets resolve as consistently and unsurprisingly as, you know, credit-default swaps or bank contingent capital securities. Which is to say: not perfectly consistently or unsurprisingly. But hopefully good enough for institutional use.

I think that, at a high level, this is roughly the approach of Kalshi, one of the two big prediction markets and the one that leans most into being a regulated US commodities futures exchange. I mean, we are in very early innings. I don’t think there’s necessarily a committee of philosophers and lawyers yet. But there are both regulatory and commercial pressures to get this stuff more or less right.

Meanwhile Polymarket, the other big prediction market, started out crypto-y, so it takes a crypto-y approach to resolving events. Crypto things love to be decentralized and do stuff with tokens, and Polymarket’s resolution mechanism is decentralized and tokenized. As the Wall Street Journal describes it:

Polymarket doesn’t resolve disputes itself. Instead, it relies on a service called UMA that runs a crowdsourced, crypto-based arbitration process for prediction markets. When a dispute arises, holders of UMA’s digital tokens debate the situation in forums on the social-media platform Discord, then vote on the outcome. UMA “governs this process to ensure fairness and transparency,” Polymarket says on its website.

Still, UMA has been a lightning rod for controversy in previous resolution disputes. Some traders have complained that the process is ripe for manipulation by anonymous UMA “whales” whose holdings of the token gives them outsize voting power.

Different individuals hold different amounts of UMA, and therefore have different voting power.

It isn’t known who the largest UMA holders are, or what might affect how they vote. It is entirely possible that the people who finally settle a bet on UMA have large amounts of money staked on it.

“It’s the protocol that you should vote the right way,” said Ben Yorke, formerly a researcher at Cointelegraph. “But [UMA] gets it wrong all the time. And there have been cases where votes are decided by, like, one or two very large UMA holders.”

And here is a Substack post on “How To Rig a Disputed Election’s Prediction Markets for $10 Million or Less,” arguing that you could manipulate Polymarket resolutions by buying up some UMA tokens, or manipulate Kalshi resolutions by bribing Kalshi. I suppose the Polymarket approach is a little bit like the resolution mechanism for credit default swaps, which does involve a vote of a committee of big CDS traders. But Polymarket’s is considerably more crypto-y.

Because prediction markets are just little babies, in some practical sense barely one year old The Bloomberg opinion article "Prediction Markets Are a Thing Now," published on November 7, 2024, argues that prediction markets have rapidly matured into a legitimate and enduring financial tool, barely one year after their mainstream breakthrough during the 2024 U.S. presidential election. It highlights their growth from niche platforms like Polymarket—where election betting volumes exceeded $3 billion—to institutional recognition, such as Bernstein analysts declaring them a "viable asset class" amid rising trading volumes and regulatory shifts. The piece discusses expanding applications beyond politics to sports and economic events, citing legal wins against CFTC enforcement (e.g., event contract cases) and potential for sports betting on granular outcomes like player stats, while noting ongoing hurdles like U.S. regulatory ambiguity. [read]; they are learning on the job and there are lots of problems to be worked out. Check back in in 10 years and everything will run as smoothly as any other financial market. (Which, again, is not perfectly smoothly!)

Because prediction markets are fundamentally different from other financial markets. Other financial markets pay $X if the trading price of Y is above $Z; the range of possibilities is narrow and susceptible to objective measurement. Prediction markets pay $1 if any possible event in the world occurs, and there will always be new sorts of events and new complications. The philosophers will stay busy, and in 10 years there will be currently unimaginable ambiguities still making resolutions controversial. “How can you say the aliens have landed when in fact they hover,” people will object in the comments, but the committee has to make a decision.

Mythos risk

Okay I’ve got a business model for Dario Amodei. Here’s what you do. You build an incredibly powerful artificial intelligence system thatUS Treasury Secretary Scott Bessent and Federal Reserve Chair Jerome Powell held an urgent meeting on April 7, 2026, with CEOs of major US banks to warn about cyber risks from Anthropic's new AI model, Mythos, which can identify and exploit vulnerabilities in major operating systems and web browsers. Attendees included Citigroup's Jane Fraser, Morgan Stanley's Ted Pick, Bank of America's Brian Moynihan, Wells Fargo's Charlie Scharf, and Goldman Sachs' David Solomon; JPMorgan's Jamie Dimon could not attend. The previously unreported session at Treasury headquarters emphasized banks' need to bolster defenses against AI-driven cyberattacks, viewed by regulators as a top financial industry threat. A Treasury spokesperson noted the meeting addressed AI's rapid developments, with attendees already in Washington for other events. [read] “is capable of identifying and then exploiting vulnerabilities in every major operating system and web browser when directed by a user to do so.” Then you hack into all the banks and steal all of their money. “It may be difficult to know what role money will play in a post-artificial general intelligence world,” you cackle, surrounded by bags of loot with dollar signs on them.

Obviously this is not legal advice and there are flaws in this business plan, though you shouldn’t overstate them. (When the police come to arrest you, you hack into their computers too and send them to the wrong address, etc.) It turns out that, so far, “artificial intelligence” seems to be better at computer programming than at most other domains of human intelligence. But being really good at computer programming is, in our modern world, pretty useful.

Treasury Secretary Scott Bessent and Federal Reserve Chair Jerome Powell summoned Wall Street leaders to an urgent meeting on concerns that the latest artificial intelligence model from Anthropic PBC will usher in an era of greater cyber risk. …

Anthropic’s Mythos is a more powerful system that the AI firm has said is capable of identifying and then exploiting vulnerabilities in every major operating system and web browser when directed by a user to do so.

Regulators’ caution about the power of the model in hackers’ hands echoes Anthropic’s own prudence. Anthropic has limited the release of it to just a few major technology and finance firms at first. Those companies, which include Amazon.com Inc. and Apple Inc. as well as JPMorgan Chase & Co., are part of “Project Glasswing,” which will work to secure the most important systems before other similar AI models become available.

Right right fine in the actual world Anthropic is working with the banks to secure their systems against other similar models, because its actual business model is mostly being an enterprise AI company. But, you know, on a blank slate you might say “well if we could send ourselves all the money that would be good.”

Robinhood Platinum

I feel like the simple model is:

What young people want, in a stock brokerage or any other service, is a well-designed app on their phone that allows them to get things done without ever talking to a human.

What old people want, in a stock brokerage or any other service, is a person they can talk to directly to get things done without ever messing around with an app.

I say this as someone who was once young and is now old. A lot of people are in my situation, though; it is in the nature of humanity that we start young and become old. If you are a brokerage, or any other service provider, you gotta keep up. Bloomberg’s Charlie Wells and Paulina Cachero report Fintech firms like Robinhood and Revolut are offering luxury perks, such as F1 race access and premium metal cards, to retain wealthy clients who have outgrown their meme-stock origins tied to young, basement-dwelling traders. These incentives target "newly rich" users by associating the apps with high-end experiences like Formula 1 events. Related coverage highlights Revolut's launch of a limited-edition titanium Audi Revolut F1 Team card, featuring aerodynamic design matching their 2026 car, plus 20x RevPoints on team merch and exclusive events like the 'OverTake: The After Party' DJ night ahead of the Melbourne Grand Prix. [read]:

Robinhood, eToro, Revolut and Public.com are often associated with twentysomethings in their parents’ basements. Now those brokerage firms are offering investors access to airport lounges, gala dinners and Formula One races. They’re rolling out $695 premium credit-cards made of precious metals, creating elite concierge services exclusively for customers with million-dollar balances and pushing into complex tax planning, wealth management and even trust accounts in a bid to compete with more established rivals. …

Revolut, a London-based fintech company, has been making strides into private banking and is planning more products targeting high-balance consumers. Revolut has also sought to hire multi-lingual private bankers to on-board high-net-worth individuals, cross-sell and give financial advice.

The pitch from Public’s chief operating officer, Stephen Sikes, is that better data, content and AI tools are making people more comfortable managing even tens of millions of dollars themselves. His firm has hired concierges to talk trading with high-value customers, build rapport with potential members and improve their experience.

Right sure you’re comfortable managing tens of millions of dollars yourself, but if you call your broker you want someone to answer.

The basic push/pull with artificial intelligence and white-collar jobs is that, if you can get an AI to do 90% of your job, you will be more productive and have more leisure time, but if your boss notices, you might get fired and replaced by the AI. There are various, like, online quizzes to help you figure out of you are more likely to benefit from this dynamic or get fired, but one simple heuristic is: If you are the chief executive officer and controlling shareholder of a trillion-dollar company, you’re probably safe. Go ahead and automate yourself. No one is going to fire you, because nobody can fire you.

Meta is building an artificial intelligence version of Mark Zuckerberg that can engage with employees in his stead, as part of a broader push to remake the Big Tech company around AI.

The $1.6tn group has been working on developing photorealistic, AI-powered 3D characters that users can interact with in real time, according to four people familiar with the matter.

The company recently began prioritising a Zuckerberg AI character, three of the people said.

The Meta chief is personally involved in training and testing his animated AI, which could offer conversation and feedback to employees, according to one person.

They added that the character was being trained on the billionaire’s mannerisms, tone and publicly available statements, as well as his own recent thinking on company strategies, so that employees might feel more connected to the founder through interactions with it.

I hope he will have his robot 1-on-1s in the metaverse, ha ha ha ha ha, remember the metaverse? I do think that “feel more personally connected to Mark Zuckerberg by interacting with an animated AI clone of him” is really the culmination of everything Facebook/Meta has worked for since its founding. In the future, most of everyone’s friends will be AI Mark Zuckerberg.

Things happen

Ackman Starts Marketing Pershing IPO to Raise up to $10 Billion. Goldman Shares Fall as Bond Trading Miss Outweighs Equity Record. Commodity traders lost ‘billions’ in early days of Iran war. Wrong-Way Bets on Oil Had a Star Trader Hundreds of Millions in the Hole. Energy Trader Vitol Reorganizes Derivatives Team After Losses. SpaceX Deal Lines Up $3 Billion in Tax Savings for EchoStar CEO. America’s New Tax Mantra: ‘The IRS Isn’t Going to Catch Me.’ Hollywood Heavyweights Sign Letter Opposing Paramount’s Deal for Warner Bros Hollywood heavyweights have signed a letter opposing Paramount's proposed acquisition of Warner Bros. Discovery, citing antitrust concerns amid ongoing regulatory scrutiny. The deal, backed by Paramount Skydance and funding from David Ellison and his father Larry Ellison, faces opposition from California Attorney General Rob Bonta over competition issues, despite apparent support from the Trump administration. Senator Adam Schiff has raised alarms about potential workforce layoffs, reduced domestic film production, higher consumer costs, and impacts on theaters, pressing Warner Bros. executives on these risks during hearings. [read]. Perella Weinberg to buy London advisory boutique Gleacher ShacklockPerella Weinberg Partners LP has agreed to acquire London-based advisory firm Gleacher Shacklock LLP to expand its U.K. footprint and enhance cross-border dealmaking capabilities. The deal, announced on April 13, 2026, aims to strengthen the U.S. investment bank's presence in the U.K. by integrating Gleacher Shacklock's expertise. Financial terms were not disclosed in available reports. [read]. Surge in Hedge Fund Money Transforms an Old Insurance Market A surge in hedge fund and institutional capital is transforming the 180-year-old reinsurance market, with alternative investments in property catastrophe coverage reaching a record $136 billion, up 18% from the prior year. This influx, primarily through catastrophe bonds and other instruments, is reshaping traditional reinsurance dynamics by providing reinsurers with new capital sources amid falling rates and competitive pressures. The trend reflects broader interest from hedge funds seeking uncorrelated returns, though it introduces risks like pricing pressures and market volatility. [read]. BISTRO, CDO, SRT. Anxious Parents Are Spending Upwards of $50,000 to Land Their Kid a Job Parents of college students are increasingly anxious about a tough job market for Gen Z graduates, leading some to spend thousands—upwards of $50,000—on early career coaching services to help secure jobs. These services provide resume optimization, interview preparation, networking guidance, and direct employer outreach, amid reports of high parental involvement like submitting applications (75% of Gen Zers) or attending interviews (51%). The trend reflects broader concerns among even wealthy families over slowed entry-level hiring, AI disruption, and poor market ratings for college seniors, prompting a shift toward professional support over family-led efforts. [read]. Molotov cocktail thrown at home of OpenAI chief executive Sam Altman A Molotov cocktail was thrown at OpenAI CEO Sam Altman's San Francisco home early Friday morning (April 10, 2026), setting the front gate on fire, but no one was injured. The 20-year-old suspect, Daniel Alejandro Moreno-Gama from Texas, was arrested by San Francisco Police after also making threats at OpenAI headquarters, including throwing a chair at its doors and stating plans to burn it down; he faces charges of attempted murder, arson, criminal threats, and possession of a destructive device. Altman responded in a blog post with a family photo, expressing love for his husband and child while hoping it would deter future attacks amid AI backlash, and later clarified on X that he did not blame critical journalism; the suspect's anti-AI manifesto listed other executives' addresses, per sources. OpenAI confirmed the incident, praised police response, and noted the suspect is in custody; an FBI raid occurred at his Texas home on Monday. [read]. When Bill Ackman Vented Over $2 Million, Fellow Billionaires Rushed to Commiserate Bill Ackman publicly vented on social media about a dispute with a former lawyer in his family office who demanded $2 million in severance pay (two years' salary) after rejecting a three-month severance package, citing an unsafe workplace. The post attracted support from other billionaires, including the world's richest man, who came to Ackman's defense on social media. The incident occurred while Ackman was simultaneously managing multiple major initiatives, including raising billions for a new stock-picking fund, taking his $18 billion hedge fund public, and pursuing an acquisition bid valued at over $60 billion for Universal Music Group. [read]. After Criticizing Pope, Trump Posts Image of Himself as a Jesus-Like Figure Based on the search results available, here's a summary of this news story: Key Points: US President Donald Trump publicly criticized Pope Leo XIV on Sunday night, calling him "weak on crime" and "terrible for foreign policy," and accusing him of being "very liberal" and overly sympathetic to the "Radical Left." About 40 minutes after his attack, Trump posted an AI-generated image depicting himself in a Jesus-like role performing a biblical miracle, shown in flowing robes with light radiating from his hands as he healed a sick man, surrounded by American flags, military aircraft, and angelic figures. The exchange stemmed from the Pope's weekend comments criticizing what he called a "delusion of omnipotence" driving global conflict, to which Trump responded by arguing the Pope should focus on spiritual duties rather than political commentary on US foreign policy and nuclear weapons issues. [read].

If you'd like to get Money Stuff in handy email form, right in your inbox, please subscribe at this link. Or you can subscribe to Money Stuff and other great Bloomberg newsletters here. Thanks!

Like getting this newsletter? Subscribe to Bloomberg.com for unlimited access to trusted, data-driven journalism and subscriber-only insights.

Before it’s here, it’s on the Bloomberg Terminal. Find out more about how the Terminal delivers information and analysis that financial professionals can’t find anywhere else. Learn more.

here

here